Suggestions based on the Question and Answer that you are currently viewing

Describe the differences between mass production and custom production of goods and services. Explain how these differences influence the costing method.

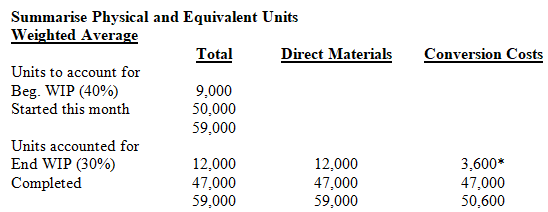

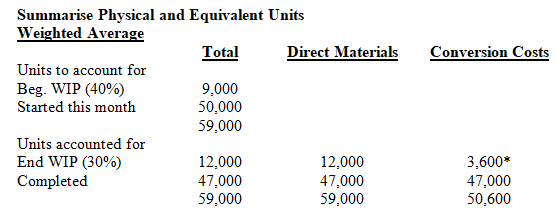

Cost of sales schedule

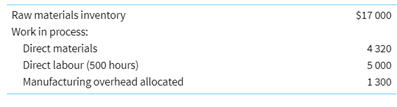

Rebecca Ltd is a manufacturer of machines made to customer specifications. All production costs are accumulated by means of a job order costing system. The following information is available at the beginning of the month of October.

A review of the job order cost sheets revealed the composition of the work in process inventory on October 1 as follows:

Activity during the month of October was as follows:

On 31 October, inventories consisted of the following:

Required

Prepare a detailed schedule showing the cost of goods manufactured for October.

Journal entries

Langley uses a job costing system. At the beginning of the month of June, two orders were in process as follows:

There was no inventory in finished goods on 1 June. During June, orders numbered 106 to 120 were put into process.

Direct materials requirements amounted to $13 000, direct labour costs for the month were $20 000, and actual manufacturing overhead recorded during the month amounted to $28 000.

The only order in process at the end of June was order 120, and the costs incurred for this order were $1150 of direct materials and $1000 of direct labour. In addition, order 118, which was 100 per cent complete, was still on hand as of 30 June. Total costs for this order were $3300. The entity's overhead allocation rate in June was the same as that used in May and is based on labour cost.

Required

(a) Prepare journal entries (with supporting calculations) to record the cost of goods manufactured, the cost of sales, and the closing of the overapplied or underapplied overhead to cost of sales.

(b) Describe the two different approaches to closing overapplied or underapplied overhead at the end of the period. How do you choose an appropriate method?

Analysis of WIP T-account

Jasper Company uses a job costing system. Overhead is allocated based on 120 per cent of direct labour cost. Last month’s transactions in the work in process account are shown here:

Only one job, number 850, was still in process at the end of the month. Job 850 was charged with $9000 in overhead for the month.

Required

(a) What is the ending balance in the WIP account?

(b) How much direct labour cost was used for job 850?

(c) What is the amount of direct materials used for job 850?

Direct costs and overhead

Job 87M had direct material costs of $400 and a total cost of $2100. Overhead is allocated at the rate of 75 per cent of prime cost (direct material and direct labour).

Required

(a) How much direct labour was used?

(b) How much overhead was allocated?

Normal and abnormal spoilage

Franklin Fabrication produces custom-made security doors and gates. Currently two jobs are in process, 359 and 360. During production of Job 359, the supervisor was on holidays and the employees made several errors in cutting the metal pieces for the two doors in the order. The spoiled metal pieces cost $20 each and had zero scrap value. In addition, an order of five gates that had been manufactured for Job 360 required a fine wire mesh that sometimes tore as it was being mounted. Because a similar wire could be used that was much easier to install, the customer had been warned that costs could run over the bid if any difficulty was encountered in installing the wire. One of the gates was spoiled during the process of installing the wire. The cost of the materials and direct labour for the gate was $150. The gate and metal were hauled to the dump and discarded.

Required

(a) Should the spoilage for Job 359 be categorised as normal or abnormal spoilage? Explain.

(b) Should the spoilage for Job 360 be categorised as normal or abnormal spoilage? Explain.

(c) Prepare spoilage journal entries for both jobs.

Job costing, over- and underapplied overhead, journal entries

Shane’s Shovels produces small, custom earth-moving equipment for landscaping companies. Manufacturing overhead is allocated to work in process using an estimated overhead rate. During April, transactions for Shane’s Shovels included the following:

Beginning and ending work in process were both zero.

Required

(a) What was the cost of jobs completed in April?

(b) Was manufacturing overhead underapplied or overapplied? By how much?

(c) Write out the journal entries for these transactions, including the adjustment.

Job Costing, determination of manufacturing overhead rates

One Glass Brewery estimates the following activity for the coming year:

At the end of the financial period the following information was collected:

Required

(a) What was the predetermined manufacturing overhead rate calculated at the beginning of the year?

(b) What was the actual manufacturing overhead rate for the year?

(c) Explain the difference between the rates calculated in (a) and (b) above.

To what extent do the costs used to value inventories for external financial reporting support internal management decisions on issues such as whether to accept a special, one-off order or whether to outsource part or all of the production process?

List the most common allocation bases used in job costing and explain under what circumstances each base would be most appropriate.

Explain how manufacturing overhead cost pools and cost allocation are related.

Exquisite Furniture designs and manufactures custom furniture from exotic materials. Explain why spoilage is sometimes recorded as a cost for a specific job and other times as overhead for this entity.

Part of a contract between a union and a company guarantees that all manufacturing employees earn five hours of overtime each week. In the company’s job costing system, should overtime be treated as a direct or indirect cost?

Within the area where you live, work, or attend school, name three businesses that would likely use job costing.

Will underapplied and overapplied overhead arise under both actual and normal costing? Explain your answer.

Compare actual and normal cost systems. Discuss the ways in which they are similar and the ways they differ.

List several different sources of information used in job costing, and explain why this information is required.

List three examples of job cost records you would receive if you were building a new home. (Hint: Itemised bills made out to you are usually job cost records.)

Describe an inventoriable product cost.

Describe the procedures used in job costing.

Two new software projects are proposed to a young, start-up company. The Alpha project will cost $150,000 to develop and is expected to have annual net cash flow of $40,000. The Beta project will cost $200,000 to develop and is expected to have annual net cash flow of $50,000. The company is very concerned about their cash flow. Using the payback period, which project is better from a cash flow standpoint? Why?

What do you think you now know that would be useful for managing projects at the hotel?

You manage a hotel resort located on the South Beach on the Island of Kauai in Hawaii. You are shifting the focus of your resort from a traditional fun-in-the-sun destination to eco-tourism. (Eco-tourism focuses on environmental awareness and education.) How would you classify the following projects in terms of compliance, strategic, and operational?

a. Convert the pool heating system from electrical to solar power.

b. Build a 4-mile nature hiking trail.

c. Renovate the horse barn.

d. Launch a new promotional campaign with Hawaii Airlines.

e. Convert 12 adjacent acres into a wildlife preserve.

f. Update all the bathrooms in condos that are 10 years or older.

g. Change hotel brochures to reflect eco-tourism image.

h. Test and revise disaster response plan.

How easy was it to classify these projects? What made some projects more difficult than others?

1. How valuable do you think being a certified PMP is?

1. If you were a student interested in pursuing a career in project management how important do you think being a CAPM would be?

The benefits of buying with AnswerDone:

Access to High-Quality Documents

Our platform features a wide range of meticulously curated documents, from solved assignments and research papers to detailed study guides. Each document is reviewed to ensure it meets our high standards, giving you access to reliable and high-quality resources.

Easy and Secure Transactions

We prioritize your security. Our platform uses advanced encryption technology to protect your personal and financial information. Buying with AnswerDone means you can make transactions with confidence, knowing that your data is secure

Instant Access

Once you make a purchase, you’ll have immediate access to your documents. No waiting periods or delays—just instant delivery of the resources you need to succeed.