Suggestions based on the Question and Answer that you are currently viewing

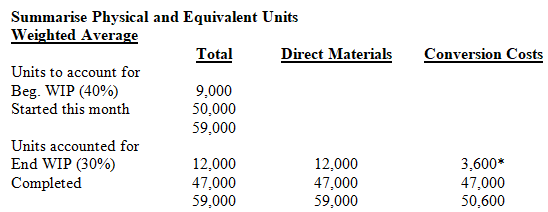

Equivalent units under weighted average and FIFO

Francisco’s mass-produces folding chairs in Port Sorrell. All direct materials are added at the beginning of production, and conversion costs are incurred evenly throughout production. The following production information is for the month of May:

Required

(a) Calculate the equivalent units used to calculate cost per unit under the weighted average method.

(b) Calculate the equivalent units used to calculate cost per unit under the FIFO method.

List three factors that managers might consider in deciding whether to expend resources to reduce spoilage.

List two factors that could affect managers’ choices for the number of times and points in processing to inspect units.

An entity has one machine through which is drawn a standard type of wire to make nails. With minor adjustments, different sized nails are produced with different sized wire. Would you recommend that the entity employ job or process costing methods?

Classification of rework costs, uncertainties, critique of rework and scrap policy

Fran Markus is in the cost accounting group at Boats Galore, a large manufacturing company that produces customised boats and yachts. The company sometimes experiences quality problems with its fibreglass raw material, causing flawed areas in boat hulls. The problem is often fixed by reworking the flawed areas. Other times the hull is scrapped because it is too flawed, and a new hull is fabricated. The spoilage policy at Boats Galore is to charge the cost of rework and spoilage to overhead unless it arises because a hull design is particularly complicated. In those cases, the cost is assigned to the job.

Two boats currently under construction require triple the amount of materials and labour time to enhance boat security. The customer wants each hull to be able to withstand the explosion of a small bomb. It is the company’s first order with this hull construction. Because of the new design and fibreglass process, the customer has agreed to a cost-plus contract and will pay cost plus a fixed percentage of cost. This contract assures that Boats Galore does not incur a loss from developing the enhanced security hull. This week, the third layer on one of the boat hulls had a flaw in the fibreglass. The area was reworked, after which it met the security requirements.

Fran receives weekly data on labour and materials for each boat under construction. For regular production, workers estimate the time and materials used to rework flawed fibreglass areas, and Fran adds those costs to overhead instead of recording them as a cost of the particular job. Now she needs to decide how to record the cost of rework for the enhanced security hulls. The production people are not sure whether the flaw was due to poor quality fibreglass or to the triple hull design. If Fran adds the cost to the job order, the customer will pay for the labour and supplies as part of the cost-plus price. If she adds the cost to overhead, the cost will be spread across all jobs and only part of it will be allocated to the job having the enhanced security hulls.

Required

(a) Critique the company’s accounting policy for rework and scrap.

(b) Describe uncertainties about the accounting treatment for the rework costs on the enhanced security hull job.

(c) Discuss the pros and cons of alternative accounting treatments for the rework costs on this job.

(d) Suppose you are an accounting work-experience student at Boats Galore. Fran asks you to recommend an accounting treatment for the rework costs on the enhanced security hull job.

i) Write a memo to Fran with your recommendation. As you write the memo, consider what information Fran will need from you to help her make a final decision.

ii) Write one or two paragraphs explaining how you decided what information to include in your memo.

Effects of robotic equipment on overhead rates

'Our costs are out of control, our accounting system is screwed up, or both!' screamed the sales manager. 'We are simply non-competitive on a great many of the jobs we bid on. Just last week we lost a customer when a competitor underbid us by 25 per cent! And I bid the job at cost because the customer has been with us for years but has been complaining about our prices.'

This problem, raised at the weekly management meeting, has been getting worse over the years. The Johnson Tool Company produces parts for specific customer orders. When the entity first became successful, it employed nearly 500 skilled machinists. Over the years the entity has become increasingly automated and now uses a number of different robotic machines. It currently employs only 75 production workers but output has quadrupled.

The problems raised by the sales manager can be seen in the portions of two bid sheets brought to the meeting (as reproduced). The bids are from the cutting department, but the relative size of these three types of manufacturing costs is similar for other departments.

The cutting department charges overhead to products based on direct labour hours. For the current period, the department expects to use 4000 direct labour hours. Departmental overhead, consisting mostly of depreciation on the robotic equipment, is expected to be $1 480 000.

An employee can typically set up any job on the appropriate equipment in about 15 minutes. Once machines are operating, an employee oversees five to eight machines simultaneously. All that is required is to load or unload materials and monitor calibrations. The department’s robotic machines will log a total of 25 000 hours of run time in the current period.

For bid 74683 the entity was substantially underbid by a competitor. The entity did get the job for bid 74687, but the larger jobs are harder to find. Small jobs arise frequently, but the entity is rarely successful in obtaining them.

Required

(a) Critique the cost allocation method used within the current cost accounting system.

(b) Suggest a better approach for allocating overhead. Allocate costs using your approach and compare the costs of both jobs under the two systems.

(c) Discuss the pros and cons of using job costs to determine the price for a job order.

Plant-wide versus production cost pools

Flexible Manufacturers produces small batches of customised products. The accounting system is set up to allocate plant overhead to each job using the following production cost pools and overhead allocation rates

Actual resources used for job 75:

The manufacturing accountant wants to simplify the cost accounting system and use a plant wide rate. If the preceding costs are grouped into a single cost pool and allocated based on labour hours, the rate would be $35 per direct labour hour.

Required

(a) What cost should be allocated to job 75 using the plant-wide overhead rate?

(b) What cost should be allocated to job 75 using the production cost pool overhead rates?

(c) Why do the allocated amounts in parts (a) and (b) differ?

(d) Which method would you recommend? Explain your choice.

Job costing; overhead rates

The Eastern Seaboard Company uses an estimated rate for allocating factory overhead to job orders based on machine hours for the machining department and on a direct labour cost basis for the finishing department. The company budgeted the following for last year:

During December, the cost record for job 602 shows the following:

Required

(a) What is the estimated overhead allocation rate that should be used in the machining department? In the finishing department?

(b) What is the total overhead allocated to job 602?

(c) Assuming that job 602 consisted of 200 units of product, what is the unit cost for this job?

(d) What factors affect the volume of production in a period? Can we know all of the factors before the period begins? Why?

(e) Explain why the company would use two different overhead allocation bases.

Accounting for scrap

You are helping a friend, Jonah, set up a new accounting system for a small start-up construction company. He specialises in custom, energy efficient homes that are built on a cost-plus basis. Cost-plus means that his customers pay a fixed percentage above the sum of direct and overhead costs.

As he goes through the accounts, Jonah asks why you set up a separate account for scrap. He does not believe that scrap should be recorded anywhere in his accounting system because it is worth little, and theft is no problem. He makes weekly trips to a recycling plant where he receives a small sum for the scrap. Most of the time Jonah is working on only one house and the scrap is only for that house. However, once in a while he is working on several houses, and the scrap for all of the houses is recycled at once.

Required

(a) Explain the two ways that scrap can be recorded in a job costing system.

(b) Choose the appropriate method for Jonah and explain your choice.

(c) Suppose you are a prospective homeowner. Explain to Jonah why you believe the revenue from scrap associated with your home should be recorded as a reduction in your costs rather than his overall costs.

(d) Write a brief (and diplomatic) paragraph to convince Jonah that he needs to account for the revenues from scrap.

Cost of rework; control of scrap; accounting for scrap

Dapper Dan Draperies manufactures and installs custom-ordered draperies.

Required

(a) For all drapes, occasionally the sewing equipment malfunctions and the drape must be reworked. Explain how to account for the cost of rework when it is needed.

(b) Explain how to account for the cost of rework when customers choose a fabric that is known to require rework.

(c) Explain why scrap will always arise in this business.

(d) Dapper Dan can sell scraps to quilting groups or just throw them away. List several factors that could affect this decision.

(e) If Dapper Dan decides to sell scraps, explain the accounting choices for recording the sales value.

Collecting overhead cost information

A family member asked you to review the accounting system used for Hanna’s, a custom stained glass manufacturing business. The owner currently uses a software package to keep track of her bank account, but she does not produce financial statements. The owner seeks your help in setting up a costing system so that financial statements can be produced on a monthly basis.

Required

(a) What kind of costing system is needed for this setting?

(b) You plan to categorise the banking data for entry into the financial statement records. List the categories you might use for these entries. List only broad categories here [see parts (c), (d), and (e) for more details.]

(c) List several costs that might be included in a fixed overhead category.

(d) List several costs that might be included in a variable overhead category.

(e) List several costs that might be included in direct materials.

(f) Write a memo to the owner discussing the alternative choices for the costing system. Include an explanation of the type of information that would need to be captured to support the costing system.

Spoilage journal entries

Jones Company manufactures custom doors. When job 186 (a batch of 14 custom doors) was being processed in the machining department, one of the wood panels on a door split. This problem occurs periodically and is considered normal spoilage. Direct materials and labour for the door, to the point of spoilage, were $35. In addition, a storm caused a surge in electricity, and a routing machine punctured the wood for job 238. This incident occurred at the beginning of production, so spoilage amounted to only the cost of wood, at $200.

Required

(a) Prepare the journal entries for normal and abnormal spoilage.

(b) Now suppose that the wood from abnormal spoilage can be sold for $25. Record the journal entries for the disposal value.

(c) Jones Company is considering hiring someone to inspect all wood after it arrives at the plant, but prior to production. Discuss the pros and cons of hiring an inspector.

Journal entries for job costing

At the beginning of the accounting period, the accountant for ABC Industries estimated that total overhead would be $80 000. Overhead is allocated to jobs on the basis of direct labour cost. Direct labour was budgeted to cost $200 000 this period. During the period only three jobs were worked on. The following summarises the direct materials and labour costs for each:

Job 1231 was finished and sold; job 1232 was finished but is waiting to be sold; and job 1233 is still in process. Actual overhead for the period was $82 000.

Required

Prepare the following journal entries.

(a) Cost recorded during production

(b) Cost of jobs completed

(c) Cost of sales

(d) Allocation of overapplied or underapplied overhead allocated on a pro rata basis to the ending balances in work in process, finished goods, and cost of sales

Allocating overhead; over- and underapplied overhead; spoilage

The Futons for You Company sells batches of custom-made futons to customers and uses predetermined rates for fixed overhead, based on machine hours. The following data are available for last year:

Required

(a) Calculate the estimated overhead allocation rate to be used for the year.

(b) Determine the overhead to be allocated to job 21.

(c) Determine total overapplied or underapplied overhead at the end of the year.

(d) Should cost of sales be increased or decreased at the end of the year? Why?

(e) If the amount of overapplied or underapplied overhead is material, how is it assigned?

(f) Suppose Job 21 required a special fabric cover for the futon pads. This type of fabric dulls the blades of the cutting machine, and a number of fabric covers were unusable. Should this spoilage be recorded for Job 21 or for all jobs processed this period? Explain your answer.

Job costing journal entries

Vern’s Van Service customises light trucks according to customers’ orders. This month the entity worked on five jobs, numbered 207 to 211. Materials requisitions for the month were as follows:

An analysis of the payroll records revealed the following distribution for labour costs:

Other overhead costs (consisting of rent, depreciation, taxes, insurance, utilities, etc.) amounted to $3600. At the beginning of the period, management anticipated that overhead cost would be $6400 and total direct labour would amount to $5000. Overhead is allocated on the basis of direct labour dollars.

Jobs 207 to 210 were finished during the month; Job 211 is still in process. Jobs 207 to 209 were picked up and paid for by customers. Job 210 is still on the lot waiting to be picked up.

Required

(a) Prepare the journal entries to reflect the incurrence of materials, labour, and overhead costs; the allocation of overhead; and the transfer of units to finished goods and cost of sales.

(b) Close overapplied or underapplied overhead to cost of sales.

When units are transferred from one department to another, how are normal spoilage costs recorded?

In processes involving pipeline operations or assembly line operations, if the pipeline or assembly line is always full, then beginning and ending WIP inventories are always 50 per cent complete with regard to conversion costs. Explain.

A department within a processing operation has some finished units physically on hand. Should they be counted as completed units or as ending inventory in the department? Explain.

Suppose the percent completion of ending WIP is overestimated at the end of year 1. How does this measurement error affect the process costing results in year 1 and year 2?

Although process costing appears to use precise measurements, it requires several estimates. Discuss where judgement is needed in collecting information for process costing.

In a continuous processing situation (such as an oil refinery), the beginning and ending WIP inventories are frequently the same. How does this simplify determination of equivalent units completed?

‘We treat spoiled units as fully completed regardless of when the spoiled units are detected. This method makes unit costing much simpler.’ What is wrong with this approach?

Under what conditions could a process complete more units during the period than it started?

Under what conditions will weighted average and FIFO process costing consistently produce similar equivalent unit costs?

Explain the difference between the weighted average and FIFO methods for process costing. Explain why an entity might choose one method over the other.

The benefits of buying with AnswerDone:

Access to High-Quality Documents

Our platform features a wide range of meticulously curated documents, from solved assignments and research papers to detailed study guides. Each document is reviewed to ensure it meets our high standards, giving you access to reliable and high-quality resources.

Easy and Secure Transactions

We prioritize your security. Our platform uses advanced encryption technology to protect your personal and financial information. Buying with AnswerDone means you can make transactions with confidence, knowing that your data is secure

Instant Access

Once you make a purchase, you’ll have immediate access to your documents. No waiting periods or delays—just instant delivery of the resources you need to succeed.